“Why are my credit scores different?” is a common question because it’s a common occurrence. You check your credit scores with one source, but then a lender says you have a different score. Or you get your credit scores from two different websites and the numbers aren’t the same. It can be confusing, so let us explain what’s going on.

There are four main reasons why your scores may be different, and we’ll explore them in more detail here:

- Bureau: Scores are obtained from different credit bureaus

- Source: The company that developed the credit score is different

- Model: The credit scoring model used is different

- Timing: Scores are pulled at different times

And then we’ll tackle the question, “What’s my real credit score?”

1. Bureau: Scores are obtained from different credit reporting agencies

The first thing to understand is that there are three major credit reporting agencies and two companies that create credit scores—mainly FICO and VantageScore. FICO and VantageScore don’t have any information about how consumers handle their bills. Instead they provide the formula used to evaluate the information in a consumer credit report. And that information comes from one of the three main consumer credit bureaus:

- Transunion

- Experian

- Equifax

These credit reporting agencies don’t share information with one another and it is possible there are differences in your reports from each of these bureaus. For example, a collection account may appear on one of your credit reports and not another. That’s why it is a good idea to review your credit reports with each of the major consumer credit reporting agencies. If you don’t get your full reports from another source, you can check them at AnnualCreditReport.com, the official free credit report website.

2. Source: The company that developed the score is different

FICO scores are the most commonly used credit scores. FICO (formerly Fair Isaac Company) started creating credit scores in the late 1950s.

In 2006, the VantageScore was created as a joint venture among credit bureaus Experian, Equifax, and TransUnion to compete with FICO scores.

In addition, each of the credit bureaus may create their own proprietary credit scores. Sometimes these are used by lenders, and other times they are “educational credit scores” offered to consumers, but not used by lenders to make credit decisions.

Finally, financial institutions may create their own proprietary scores that are not available to the public. They may use information from one of the credit reporting agencies but also customize the score to their customer base. These are often referred to as “custom scores.”

Each score is intended to measure a certain type of risk of a borrower based on information in their credit report. But each one may approach the analysis in a somewhat different way. That means you can get your credit score from the same bureau the same day and the actual number may be different depending on whether it’s a FICO score or VantageScore.

3. Model: The credit scoring model used is different

There is no single FICO score. They come in different versions, referred to as “models.” These scores are updated over time, and some credit scoring models are used for specific types of lending such as auto loans or bank cards (general purpose credit cards.)

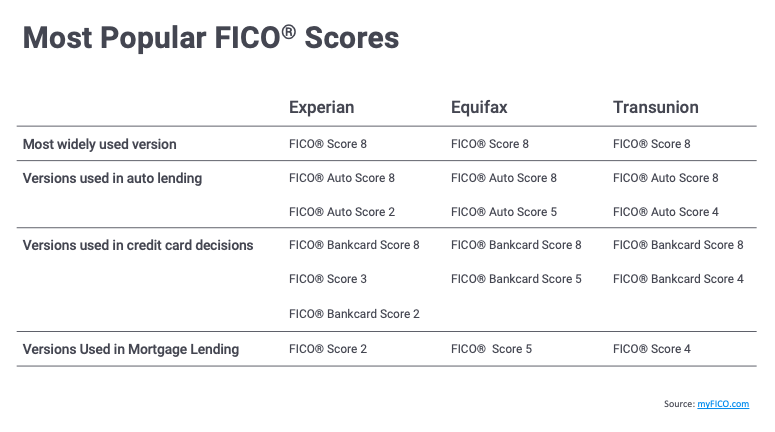

Which credit scores do lenders use?

This chart from MyFICO.com illustrates different credit scoring models most commonly used (FICO score only):

As you can see, different scoring models may be used by mortgage lenders, auto lenders and card issuers. You can also see how different models are available through each bureau. For example, for mortgage lending, lenders are likely to pull a FICO Score 4 from TransUnion, a FICO Score 2 from Experian, and a FICO Score 5 from Equifax.

VantageScore, by contrast, has four score versions and 4.0 is the latest version. If you are using a credit monitoring service to view your VantageScore, you are likely to see a VantageScore 3.0.

The 5 Main Credit Score Factors:

- Payment History (35%)

- Debt Utilization (30%)

- Credit Age (15%)

- Credit Inquiries (10%)

- Types of Credit (10%)

These factors are included in most credit scoring models, but the weight they carry (in other words, how much they impact your scores) varies by scoring model.

Payment History: Late payments hurt your credit scores. The more recent the late payment, the more it affects your scores, and the greater the number of late payments, the more they affect your scores. (A recent late payment can drop your score as much as 100 points!)

With FICO scores, this factor generally makes up around 35% of your score.

With VantageScore 3.0, it’s the top factor but with VantageScore 4.0 it’s “moderately influential.”

Debt: Revolving debt is also a substantial factor and it is heavily weighted toward credit card debt. There are different ways this factor may impact your scores. With FICO scores, this factor commonly looks at “debt utilization” “credit utilization” or “debt usage” (all terms for the same concept.) It compares your credit balances to your credit limits on your revolving lines of credit such as credit cards.

For example, if you have a credit card account with a $5,000 limit and have a $1,000 balance, your utilization or debt usage ratio is 20%. (Divide the balance by the credit limit.) This is measured both for individual revolving accounts and as an aggregate of all revolving accounts. Higher utilization ratios may impact your credit negatively. This factor is one that can change quickly: pay down a high credit card balance and your credit scores may improve as soon as the new balance is reflected in your credit reports.

With FICO scores, debt usage typically accounts for about 30% of the score.

With VantageScore 3.0 debt usage accounts for about 20% of the score, while total balances/debt accounts for about 11%. With VantageScore 4.0, total credit usage, balance and available credit are together the top factor considered “extremely influential.”

It’s worth noting that some business credit cards report to the owner’s personal credit, which means that high balances due to business activities can impact the owner’s personal credit.

Types of Credit: This factor measures credit mix, or credit diversity, in terms of the types of accounts. If your credit report shows that you have a few credit cards, a car loan, a student loan, and a mortgage, for example, you will likely have a higher credit score than someone who only has one credit card and a personal loan.

With FICO scores, credit mix accounts for roughly 15% of your credit score.

With VantageScore 3.0, age and type of credit together account for about 20% of the score, and with VantageScore 4.0 credit mix and experience are the second most influential factor, considered “highly influential.”

Credit Age: Credit age evaluates the length of credit history. It indicates how long you’ve had credit and is measured by looking at your oldest account, youngest account and the average age of all your credit accounts. The older your credit, the better. New accounts can lower your average credit age.

With FICO scores, this factor accounts for roughly 10% of your credit score.

With VantageScore 3.0 age and type of credit together account for about 20% of the score, and with VantageScore 4.0 age of credit is the next to last factor, considered “less influential.”

Credit Inquiries: Credit inquiries refers to requests for your credit reports/scores – a.k.a. “inquiries.” Hard inquiries typically drop scores by 3-5 points though that range can vary slightly. While inquiries stay on your credit reports for two years, they typically only affect your scores for one year.

Not all inquiries affect your credit scores the same way, so make sure you understand how inquiries work if you are concerned about this factor.

With FICO scores, this factor accounts for roughly 10% of your credit scores.

With VantageScore 3.0 it’s around 5% and with VantageScore 4.0 it is the least influential factor.

FYI: Checking your credit scores with Nav is a soft inquiry and does not impact your personal or business credit scores. In addition, most lenders evaluating applications for small business loans often use a soft credit check on the owner’s personal credit initially. If the owner decides to proceed with the loan there may be a hard credit check.

As you see from this description of the score factors, the same information may have a different impact depending on which credit scoring model is being used.

4. Timing: scores are pulled at different times

Credit reports are updated all the time. A credit score is created based on current data from the credit reporting agency that was used to create the score. Because credit reports are real-time, it is possible for your credit score to change from one minute to the next depending on what is being reported. For example, if you have paid your credit card bill and as a result, your revolving credit balance has dropped significantly, your score can change as soon as that new balance hits your credit reports. In this example, it is possible to see a significant score change depending on how much debt has been paid off.

Why your credit scores can be significantly different

If your credit scores are significantly different, you can first look into the reasons above to determine why. But the most common reason for a large gap is that one of the credit bureaus has information the others do not. If that information is negative— a collection account is a common example— that may result in the credit score from one credit bureau being very different from the others.

Review your credit reports carefully to see if there are accounts or other information that does not appear on your reports with the other major credit bureaus.

Which score is my real credit score?

It’s logical to wonder which score is best. The answer, though, is that the only score that really matters is the one the lender uses to evaluate the loan application for the financing you want. Typically you won’t know which particular consumer reporting agency or scoring model the bank, credit union or other type of lender will use to make a lending decision. (In a few cases, such as a mortgage application, the lender will obtain multiple credit scores from different bureaus.) So your best approach is to understand the main scoring factors and work to make each as strong as possible.

What’s a good credit score?

Most consumer credit scoring models run from 300— 850 though there are some used less often that have a different score range. Each lender determines which range is acceptable, and which score ranges help a borrower qualify for the best terms. So again, there’s no single score that’s considered “good.” However, myFICO offers a credit score calculator that helps you understand the average interest rate by credit score range. If you are shopping for a consumer loan, it can be helpful.

What is the most accurate credit score?

This is a difficult question to answer, as you’ve learned. Different credit scores are designed to evaluate creditworthiness in different ways. Ultimately, though, a credit score is only as accurate as the information used to calculate it. That means it’s essential to review your credit reports to make sure they are accurate. If they are not, you have the right to dispute information.

What to do if there are errors on your credit report

You have the right under federal law to dispute information in your credit report you believe is inaccurate or incomplete. You can dispute errors on your credit reports in one of several ways:

- Online directly with the credit bureau reporting the mistake

- By mail directly with the credit bureau reporting the mistake

- With the lender/company reporting the wrong information

Each method has pros and cons. Disputing online is fast and efficient, and you can often get a response quickly. Disputing by mail can be best for situations where you need to include extensive documentation. And disputing directly with the lender/company reporting the information means that if the company makes a correction, they will need to report that to all the credit bureaus that have the wrong data.

How to improve your credit scores

If your credit scores are keeping you from being approved for the small business financing you need, you may need to work on repairing your credit. There is a lot that can be written on this topic, but here are a few essential tips:

Step 1: Identify what’s bringing down your scores. The main factors affecting your credit scores are provided when you request your credit scores. Review them carefully.

Step 2: Identify where you can make improvements. Can you pay down credit card balances? Refinance with a personal loan? Negotiate with a collection agency to stop reporting an account if you pay it? The steps you can take will depend on what’s impacting your credit scores and whether that information can be changed. (Most negative information can be reported for seven years.)

Step 3: Build strong credit references going forward. Make sure you have at least a couple of accounts currently open and reporting to the major credit bureaus. Pay them on time each month and keep balances low.

Step 4: Monitor your credit. Improving your credit takes time. With credit monitoring, you can track your progress over time.

Conclusion

As you can see, the answer to the question “why are my scores different?” can be complex. The bottom line is that you should make sure the underlying credit information is correct on each of your credit reports.

Free credit reports and free credit scores will help you monitor the information on your credit. (Make sure you’re checking with all the major credit reporting bureaus.) Keep in mind that a credit freeze may inhibit your ability to check your reports or scores from certain sources.

Staying on top of your credit using the resources listed here can not only help you identify problems as well as build credit to get the financing you need.

This article was originally written on December 4, 2019 and updated on January 10, 2022.

My score is higher. Let’s get this together. Stay current with the numbers.

I have never received a loan for my business and it’s not fair to me that my score is low due to a mistake on my report about a loan!!!

I didn’t open that account so why are my score dropped

Lauren – if an account appears on your credit report that you didn’t open it could be due to ID theft.

Hello i would like to know is the personal score on here are accurate? Because it’s showing very high on here vs on Experian app that I have. It just updated on Friday so i just want to know if that score is accurate.

The score shown on your Nav account is supplied by Experian. It is a VantageScore 3.0. It’s confusing no doubt but as we tried to explain in the article it can depend on the score model used and even the date the score is calculated as balances or other information can change.

Some things on my report is not true how do I get them removed

You will need to contact the credit bureau to dispute it. If it is your business credit report and you have a Nav account, you are welcome to reach out to customer support and they can provide you with details on how to dispute it.

I would love to know what mw 3.0 credit score is and to keep track of it

I don’t know what a mw 3.0 score is…?

Hello I’m trying to build my business score. I have a dnb score of 53 trying to figure out how I can see why its low its says I have 28 days after term is there a way to correct or see what accounts is being reported late on the business side but my experian business is high 86 and how could you dispute something on your business file

Geno – Business credit reports don’t list the name of creditors; they don’t have to and unfortunately they choose not to. As far as disputes go, if you have a Nav account (it’s free) feel free to reach out to our customer support team atsupport@nav.com and they will do their best to answer your questions.

I’m trying to rebuild my personal credit to buy a house and start my business credit journey. I applied for an eidl loan and they denied me for open bankruptcy. This was 2004 it was discharged 2015. Experian has the proper info but my Experian personal credit says it’s open, not discharged. Why? Do I have to pay to fix this Inaccuracy? Do you have any advice on my first business credit card or steps to building my business credit? Thank you in advance

Mourey – I’d recommend a couple of things:

1. Dispute the open bankruptcy with Experian. If you have a copy of your discharge papers you can supply those but they aren’t required to file a dispute. (It just might expedite the correction.) You don’t have to pay for that.

2. Once it is corrected, apply for reconsideration for your EIDL loan.

3. To start building business credit in the meantime, you can get vendor accounts and/or a paid Nav account. You’ll find vendors that report to business credit but don’t check personal credit at Nav.com/vendors

I hope this helps!

Another question what is the form or way i send the credit bureaus the history of me paying rent on time or period?..

D&B offers a Credit Builder service that can add that information for a fee. The other way to do that, Frank, is through a service like this: This New Service Can Help You Build Business Credit Faster

I was told by a realtor credit advisor about building my credit with a card. By simply paying that card at a specific time. A cycle time and it will majorly impact for a good score. is this true and whats the cycle time?…

I wonder if they were referring to debt usage. If your balances reported to the credit bureaus are high on one or more credit cards, it may be beneficial to pay them before the close of the billing cycle so the balance that is reported is lower. What is your normal debt usage on your credit cards? (Your credit monitoring service, like Nav, should tell you that.)

I have a 640 a 632 and 574 I have paid off debt and had many things removed so why are my scores so inconsistent?

I assume you are saying those scores are from the three bureaus, Equifax, Experian and TransUnion? Then one explanation is the data and the other is that they are all three showing you scores using different scoring models. I find my own scores fluctuate from bureau to bureau as well.

Also my other question is why is my vantage score 798 with Nav but in credit wise and other apps my vantage score is 807 and my FICO score is 810?…I’m not understanding.

Chris – it can be confusing! Creditwise pulls data from TransUnion while Nav pulls data from Experian in our free account. (If you have a Nav premium account you’ll also see a score based on TransUnion data.) Remember credit scores are only calculated when they are requested, and a fluctuation of up to 20 points is not considered unusual or significant. So even if your VantageScore were pulled from the same bureau but on different days it could vary, depending on the available data on that date. (Creditors are reporting throughout the month.)

FICO uses a slightly different formula.

If this still doesn’t make sense, let us know and I’ll continue to try to help clarify it for you.

BTW, all those scores are excellent so you should be qualifying for the best rates!

Nav pulls from Experian..ok I’m 807 on Experian but still only 798 on Nav that uses Experian’s data…I’ve been over 800 for quite some time now and I still don’t understand what you’re talking about…you’re saying if you pull from different days my score can be different?…in the past year my score has only changed for 804 to 807 so I’m not sure what day Nav checked it at 798???

Chris,

Yes, pulling a credit score on a different day can make a difference. A credit score is calculated on the date it is requested based on the data available at that time. Lenders provide updates throughout the month, though, on different dates.

Most sites that provide free credit scores will pull an updated score on a specific day each month. So your score will reflect the data available on the date your credit monitoring account updates.

So let’s say you set your Experian account up on the first of the month and your Nav account on the 10th of the month. Your credit card issuer provides an update on your balance on the 5th. When you pull your score through Nav on the 10th it will include the balance your card issuer updated on the 5th. But the score Experian shows you will not reflect that new balance until it updates the following month on the first of the month. (Or vice versa).

Is that clearer?

And again, while I know it’s frustrating, your scores are all excellent– even at 798– and should be earning you the best rate.

your not speaking about Experian he is speaking of is the Fico score model 8…totally different than fair issac …that would be my answer…and yes different reporting times and pull allso like you said

Why is it that only my credit card data shows up on Nav which is powered by Experian data but when I log into Experian app it also shows my lines of credit?…my lines of credit are reported to all 3 credit agencies…and this happens to be the case with all of these third party apps that I use..lines of credit don’t show up..only credit card information…please help me to understand this.

Chris, I am not sure what you’re looking at (personal or business credit, free or premium Nav account)? But our customer support team would be happy to talk with you. They can review your data with you and answer your questions in more detail.

Child support is payed directly from my pay check. Yet every month they mark on my credit that I didn’t pay! I have all the proof that I been paying. What can I do to get my credit score back?

John, Have you tried filing a dispute with each of the credit reporting agencies that are reporting the incorrect information?

I’m so upset that my credit score went down from fro. Signing up with you guys…can I get my credit back please I’m so disappointed because I was not told that thT would happen

Jarrell – Reviewing your personal credit through Nav creates a soft inquiry on your credit report. Soft inquiries are not transmitted to lenders and do not impact credit scores. If there’s something else you observed, feel free to reach out to our Credit & Lending Team and they’d be happy to review your credit situation with you.

My credit score did not go down.

I’m starting my credit over from a bankruptcy in 2013 with a VISA from a local Credit Union. I knew going in that I was only going to use about 7% of my debt utilization which wasn’t much. I opened with a $500 limit and I used $35. Four days before the end of the month my mother went in for surgery and I decided to fly up to be with her. I rented a car and the rental company put a totally refundable hold on my card of $200 putting my balance at $235 and upping my debt utilization to 47%. The Credit Union reported to the bureau my balance on either the 30th or 1st of the month which inturn totally wrecked my plan of keeping my utilization down around 7%. On the 2nd the rental car company put the $200 back and I had already paid the $35 back from a transfer from my checking. Bottom line I went from a 601 score to a 588. It’s not a lot but it goes to show, intentions don’t mean a thing. Timing is everything. My balance is at zero and I still failed. There seems to be no account for circumstances. I used the credit card so as not to have to put up an $800 deposit on my debit card, as a credit card waived that. What’s upsetting to me is that the car rental person told me they wouldn’t charge the card, but in reality they did and now I’m paying a price of a lower score. Live and learn I suppose.

Mark,

Sorry to hear about the setback. Once you pay that off and the issuer reports the new balance, though, any credit score calculated should use the new balance. Have you seen it rebound?

I am behind you on this. While it may seem to benefit the consumer to have “real time” reporting or “real time” credit scores–it just just the opposite. To make matters worse, it really screws over the little guy trying to crawl out from under a financial debacle. It does the consumer no good whatsoever, to devise a plan for reporting credit, that you can turn around and modify in ways you choose for reasons you see fit. Credit has only served the wealthy elite for some time. Even if the average consumer had the time to figure out how to time their payments so it favored their score, or chose the best day of “their month” to apply for credit, or pay off that pesky credit card, they don’t. And quite frankly, it’s an exercise in futility to even try. And only people who don’t hold the world on a financial string are the ones who are held down and strangled by the rules made to govern such a system. If only to keep to keep an underclass as a place to collect money from, why else does one exist?

“We expect the most from those who have the least.” Period.

I coined that phrase–share it to anyone who will listen. I have yet to encounter a situation where it does not apply.

But, I do wish you all the luck in the world in staving off this coveluted system. I never said I wasn’t going to do anything about it, except to complain. No, real change doesn’t happen in the bystanders box. I am with all you little guys out here trying to keep the dirt out of my credit box. I fail more than I succeed on some days. But, I am succeeding enough to keep fighting.

“Carry on, then ……give ’em hell til they change their ways!”

May be scores are old, new score should be higher.

Ive heard utilization isnt a major factor when it comes to buisness credit , is this true. Furthermore, how can in remove hard inquiries from my business credit report. I do have nav business boost. Thanks look forward to your response

It depends on the model Keith. Experian does look at utilization while D&B Paydex does not. There is not really such a thing as hard or soft inquiries with business credit. Keep in mind that it is completely unregulated and there is no law that limits how long business inquiries may be reported, how quickly disputes must be investigated etc. Anyone can check business credit so it will be hard to state that an inquiry is unauthorized. (You can try disputing them but I think the gain would likely be minimal.) The main thing to focus on with business credit is accounts that report and paying them on time.

This credit score is over 3 years old. My credit score very high… you pull soft pull from 3 years ago base my lending power on 2013 and not on 2018. Very disappointed.

Ms. Mabins,

I am not sure I understand your comment. Do you have a Nav account? If so, then yes, it will always be a soft pull as checking your credit through Nav will not affect your credit score. I don’t know what you mean about lending power on 2013. When you log in to your Nav account you can refresh your credit score monthly. It will be based on the current information from the credit reporting agencies. We can’t base a credit score on 2013 data.

If you still have questions about your Nav account, our customer support team is available to talk with you on the phone. They’re there to help.

Why did my score decrease?

It’s impossible to say without knowing more? Are you monitoring your credit through Nav? If so you can look at your alerts for more details. If through another service you’ll need to see what information they suggest. I’m sorry I can’t be more specific,

I want to see who I have credit lines with

Marilyn,

Are you talking about personal or business credit? Both should be available in your Nav account (provided those lenders report). You can get a free Nav account here.

How can I get my personal credit score increased?

Liora,

I will be sharing strategies for business and personal credit scores on an upcoming SCORE webinar.Register here – even if you can’t attend live you will get the recording.

2 years on time debt repayments, <10% revolving credit ultilization!!! 65% of score! If you have Collections accounts, they're not as bad as late payments! But, try 50% and deletion offer! If they don't delete on offer, forget trying! Lots of new credit, I have 10 lines opened less than 14 months, with one collections account… These new accounts are eating up Collections account weight! I'm at 745, 740, 765 vantage scores now!

New credits lines cost 35 points, but rebound 30 points when under 10% ultilized, after 4 months… All 2018 year, I've opened 2-3 credit accounts every 4 months when score rebounded back to 720+! All new accounts must be opened within 2 weeks! They say within a month! But, when opening 3, your latest creditor may instantly report to credit agency? Installment loans, debt, not a big deal, their weight averages 4 points per 1000! Unless it's a home loan mortgage! It does seem a home loan mortgage carry other type of weight!

9-10-18 . Has the bankruptcy files in 9/2008 gone off my credit report, if not when?—-thanks Roger

Roger,

Are they personal bankruptcies or business bankruptcies? Personal bankruptcies should be gone by now. They usually stop reporting a month or two before the seven or ten year time period expires. (7 years from filing date for Chapter 12 and 10 years for Chapter 7).

There is no legal requirement to remove business bankruptcies after a certain period of time but as a matter of practice they will probably no longer be reported.

Have you checked your personal and business credit? If you don’t have a Nav account you can get a free Nav account here.

The great thing about the new year is its a great benchmark for change. I’ve started paying down credit cards with the intent to raise not only my score but also my credit limit. I too opened a secured card last year and a small line of credit. I appreciated the article pointing out the benefits of keeping balances at 20%, and the discipline required to do so. I have added this goal to my credit plan…thanks!

That’s great! Let us know how it goes for you.

Great information. I have learned much over the last 2 years, and one key point that the article mentioned was that not all of your creditors report to all three bureaus, so where you may see an item on TransUnion and Experian, it may not be reported to Equifax, so your scores should be close but not exact. If they are not close, you may have some outstanding item on the lowest scoring bureaus report that may not belong. Check your reports and see if that is the case, and start the dispute process to get rid of them.

I battled with my credit scores for years, until i decided in Jan 2014 to get serious, learn the REAL truth about how to fix it, and then execute. The catalyst for that was applying for credit to buy new windows for my home and being denied with a score of 560. Since a denial affords you the opportunity to get a free credit report from the denying bureau, I got that done and saw some things that were not accurate. An appeal to the bureau disputing that item got that one fixed.I also saw some things that WERE accurate and fixing those required some planning and execution on my part. I am quite proud to say that when I bought a new to me car last week my score, 22 months later, was 711.

I accomplished this by first making myself aware and evaluating my situation. I then made a plan, and step one on that plan was to get a secured credit card. I got that card, with a $200 limit (for a $49 deposit), and began using it to exactly 10% of the limit every month. I put exactly $20 worth of gas in my car, and paid it to $0 after the monthly closing but before the due date. Soon after (4 months) that card limit was increased to $500. I continued on the plan of spending 10% of the limit and paying it to $0. Slowly things turned around to a point where I went from $0 credit line to $18,500 over 8 different accounts. Of that $18,500, I NEVER charge more than 20% of it, and usually keep it down to 10-12%.

This may require some discipline on your part, whether that is putting off a vacation for this year or not buying the new 70″ TV until one year from now, but if your credit matters, and you want to fix it, you can do it. Read the blogs here at nav.com and apply what you learn, and you too will be a success story!

Thanks for sharing your experiences in so much detail, and congrats on the progress with your credit and financial life!

Thanks for the information and what worked for you!!